- Joined

- Jan 17, 2012

- Messages

- 4,541

- Reaction score

- 50

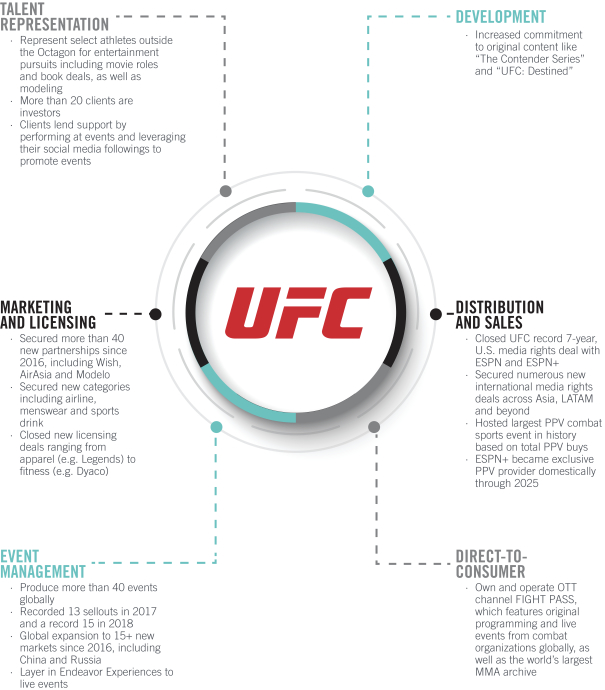

"Since acquiring UFC in 2016, the 25-year-old organization has achieved strong growth across live events with a record 15 sell-outs in 2018 across a host of new markets; enhanced media rights including a record deal with ESPN and ESPN+ in the U.S. and numerous new international media rights deals; sponsorship and licensing with more than 40 new partners; original content via its streaming service FIGHT PASS; and talent integration from across the Endeavor platform. With more than 300 million fans, including over 80% of fans outside the U.S., and one of the youngest (e.g. 40% millennials in the United States) and most diverse demographics in all of sports, UFC continues to sell out some of the biggest and most prestigious arenas around the globe, while broadcasting in over 160 territories to approximately 1 billion households."

https://www.sec.gov/Archives/edgar/data/1766363/000119312519155034/d681105ds1.htm#tx681105_12

this is also in there

"UFC has five related class-action lawsuits filed against it in the United States District Court for the Northern District of California between December 2014 and March 2015 by a total of eleven former UFC fighters. The complaints in the five lawsuits are substantially identical. Each alleges that UFC violated Section 2 of the Sherman Act by monopolizing the alleged market for the promotion of elite professional MMA bouts and monopolizing the alleged market for elite professional MMA Fighters’ services. Plaintiffs claim that UFC’s alleged conduct injured them by artificially depressing the compensation they received for their services and their intellectual property rights, and they seek treble damages under the antitrust laws, as well as attorneys’ fees and costs, and injunctive relief. UFC believes the lawsuits are meritless and therefore intends to defend itself vigorously against the allegations in the complaints.

In addition, from time to time, we are involved in disputes or litigation relating to claims arising out of our operations. While management currently believes we are not party to any legal proceedings that could reasonably be expected to have a material adverse effect on our business, financial condition and results of operations, legal proceedings are inherently uncertain."

They are under five lawsuits from fighters regarding the UFC monopoly.

and

"In 2016, Endeavor, together with affiliates of Silver Lake Partners and affiliates of Kohlberg Kravis Roberts & Co. L.P. (“KKR”) and certain other investors, acquired Zuffa Parent, LLC (“UFC Parent”), which owns and operates UFC, the world’s premier professional mixed martial arts (“MMA”) organization (the “UFC Acquisition”). We have a controlling financial interest over the business and affairs of UFC Parent and have consolidated UFC Parent’s financial results from the date of the UFC Acquisition. We currently own 50.1% of UFC Parent’s common equity."

"Our control of UFC is subject to certain consent rights held by other equityholders of UFC, whose interests in UFC may be different than ours and yours, and the terms of the preferred units issued as partial financing for the UFC Acquisition contain negative covenants that may limit our ability to pursue our business strategies with respect to UFC."

"While not participatory in nature, these rights held by the other owners of UFC limit our ability to make unilateral decisions about the management and operation of UFC without the approval of its other owners, whose interests may not be fully aligned with ours and yours, which could lead to actions that are not in our and your best interest."

So basically even though WME, now known as Endeavor, owns 50.1% of the UFC, they do not really control it. there is an entire list of things requiring the "minority" shareholder approval.

"(ii) after February 18, 2019 but prior to August 18, 2021, an initial public offering of UFC may be requested or approved by at least one director designated by each of us, Silver Lake Partners and KKR, provided that a request or approval by any two of the directors designated by each of us, Silver Lake Partners and KKR is required if the valuation in the offering achieves a specified valuation, provided that the approval of the director designated by us is required under all circumstances prior to August 18, 2021, so long as we hold a majority of the equity entitled to appoint directors of UFC, and (iii) after August 18, 2021, any of us, Silver Lake Partners or KKR, subject to certain ownership requirements, may exercise a demand right with respect to an initial public offering without approval by us or our director designees."

this means that the investors can force the UFC to undergo its own IPO by my reading. so after Endeavor IPO, it will spin off the UFC as its own public company and either sell its stock or retain ownership.

and then there is this gem.

"UFC Preferred Units

As part of the UFC Acquisition in 2016, UFC issued $360 million of preferred equity in the form of Class P Units. The holders of Class P Units are entitled to a cumulative distribution at an annual rate of 13.0%, payable quarterly in arrears by accumulating and compounding to the liquidation preference (the “preferred return”). The holders of the Class P Units have the option after the fifth anniversary to switch the rate of the preferred return from the fixed rate of 13.0% to a floating rate of 10.0% plus the five year treasury rate. The fixed rate of 13.0% and the fixed portion of the floating rate of 10.0% increases incrementally by 1.0% after the seventh anniversary, 1.0% after the eighth anniversary and 0.5% after the ninth anniversary. After the third, fourth and fifth anniversary, the Company may elect to redeem any or all of the outstanding Class P Units at an amount per unit equal to the then current liquidation preference, plus a redemption premium of 105%, 102.5% and 100%, respectively.

The Class P Units are subject to certain negative covenants that restrict, among other things, UFC’s ability to repurchase or redeem equity, make certain restricted payments, issue preferred equity, incur indebtedness and enter into affiliate transactions. The terms of the Class P Units also contain events of default, including failures to make required distributions on the Class P Units.

The negative covenants for the Class P Units restrict our ability to make distributions from our UFC subsidiaries to the Company, and therefore limit our ability to receive cash from our UFC operating units to make dividends to the holders of our Class A common stock. Generally, the Class P Units prevent any distributions to the Company except for (1) amounts necessary to make tax payments, (2) a limited annual amount for employee stock repurchases, (3) a limited amount for earn-out payments relating to the acquisition of UFC, (4) distributions required to maintain the parent entities and (5) other specific allowable situations."

This means that the stock in the UFC that WME owns can never pay dividends because the private equity stock has a 13% dividend that is cumulative. Cumulative means that if it is not paid, it is owed in the future. The WME purchase of the UFC was even crazier than anyone thought.

i wish Frankie was here to write us a nice report on this.

Last edited:

(2).gif")